Bursting the $2 Trillion SpaceX Bubble: A Value Investor’s Reality Check on IPO ROI

By Khawar Nehal, Value Investor

June 9, 2026

Not sorry to burst your bubble, but the fervor surrounding SpaceX’s anticipated IPO reads like a classic playbook we’ve seen before. It looks exactly like the Facebook valuation strategy, where a founder strategically sells a mere 1 percent of the company at a huge, headline-grabbing price to set an astronomical anchor, while the rest of the market is left to price in unrealistic, perpetual hyper-growth.

SpaceX is undeniably an engineering marvel. Elon Musk and his team have revolutionized aerospace. But as a value investor, I must separate the brilliance of the product from the mathematics of the investment. Engineering marvels do not automatically translate into sound investments at any price.

When whispers of a $2 trillion valuation dominate the 2026 IPO landscape, we must ask a fundamental question: What kind of Return on Investment (ROI) can an investor realistically expect, and how long will they have to wait for it?

Let’s run the numbers.

The Law of Large Numbers and the $2 Trillion Anchor

At a $2 trillion market capitalization, SpaceX is no longer a scrappy startup; it is priced like a mature, dominant global monopoly. To justify a standard value investor’s target of a 10% to 15% annualized return (CAGR), the company doesn’t just need to grow—it needs to generate staggering amounts of absolute free cash flow.

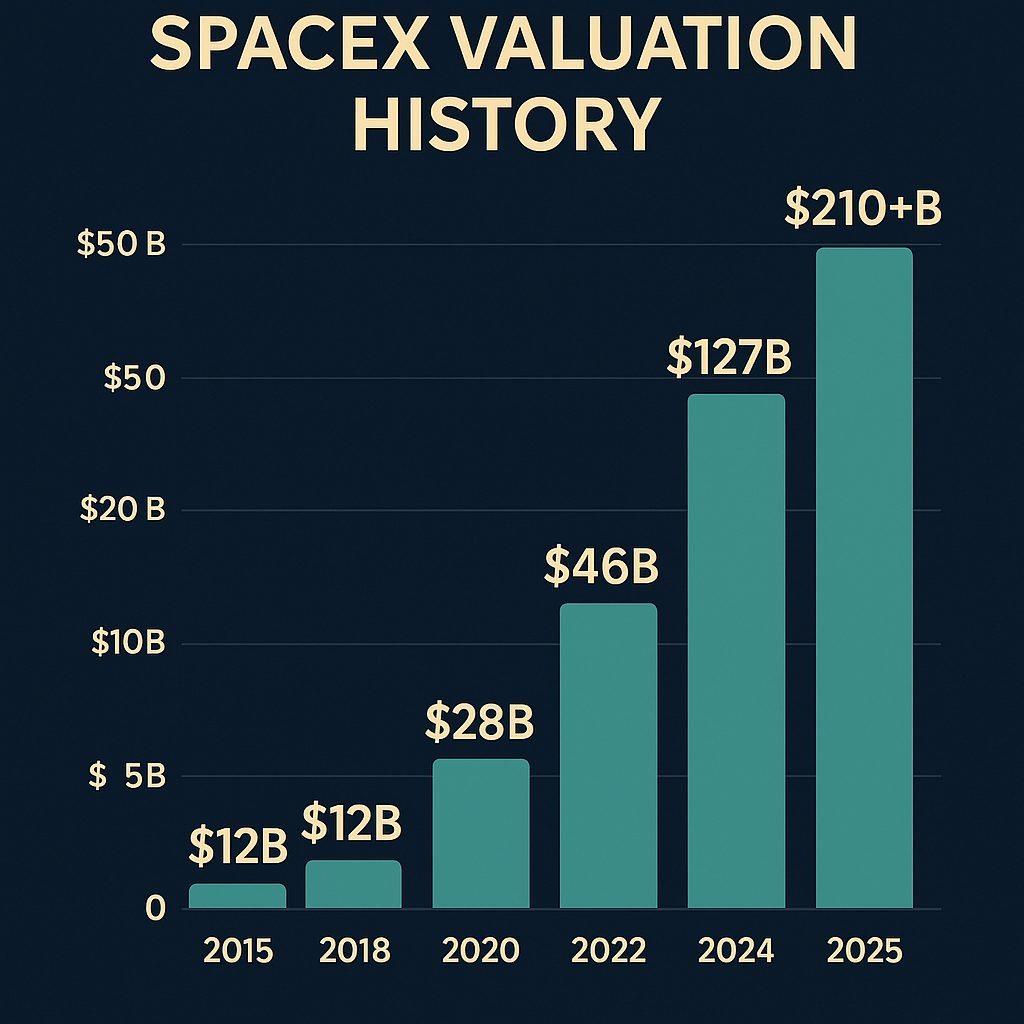

Remember, SpaceX reportedly posted a net loss of $4.9 billion in 2025. To bridge the gap between current losses and a $2 trillion valuation, the market is pricing in flawless, decades-long hyper-growth with zero margin for error.

Here is a realistic breakdown of the minimum, average, and maximum ROI an investor can expect over a 10-year horizon, even granting SpaceX the benefit of the doubt on its growth trajectory.

1. Minimum Expected ROI: The Value Trap (5% – 7% CAGR)

• The Scenario: Hyper-growth inevitably collides with the law of large numbers. Revenue growth decelerates to 10% annually. Net profit margins stabilize at a respectable but unspectacular 10%.

• The Multiple Compression: Because the company is no longer “hyper-growth,” the market re-rates the stock from a speculative 100x revenue multiple down to a mature aerospace/tech multiple of 20x.

• The Result: The $2 trillion valuation stagnates or grows to roughly $2.5 trillion over a decade.

• The ROI: A total return of 25% over 10 years. After inflation and opportunity cost, this is a wealth-destroying investment. You took on massive IPO volatility risk for the equivalent of a low-yield bond.

2. Average Expected ROI: The Reality Check (8% – 10% CAGR)

• The Scenario: SpaceX executes well. Starlink achieves global dominance, and launch services maintain their monopoly. Revenue grows at 15% annually, and net margins expand to 15%.

• The Multiple Compression: The market acknowledges the success but still compresses the valuation multiple from ~90x down to a more rational 30x as growth naturally slows.

• The Result: The market cap grows from $2 trillion to roughly $3.5 trillion over 10 years.

• The ROI: A total return of 75% over a decade. While not a loss, a 7.5% annualized return from a company billed as the greatest “hyper-growth” story of our generation is deeply underwhelming. You would have been better off in a diversified S&P 500 index fund with a fraction of the idiosyncratic risk.

3. Maximum Expected ROI: The Unicorn Case (12% – 15% CAGR)

• The Scenario: Everything goes perfectly. SpaceX captures the entirety of the global satellite internet market, Mars colonization initiatives begin generating tangible commercial revenue, and the company achieves a stellar 20% net profit margin while maintaining 20% top-line growth.

• The Multiple Hold: The market remains enamored, allowing the company to hold a premium 40x earnings multiple.

• The Result: The market cap balloons to $5 trillion to $6 trillion over 10 years.

• The ROI: A total return of 150% to 200% over a decade (roughly 10% to 12% CAGR).

Notice the catch in the “Maximum” scenario? Even if SpaceX executes a flawless, once-in-a-generation hyper-growth run for ten straight years, the ROI is merely a 2x or 3x return. In the world of value investing, waiting a full decade to double your money on a highly volatile, single-stock IPO is not a triumph; it is a mediocre outcome for the risk assumed.

The Aramco Precedent: The $2 Trillion Mirage and Desperate Stunts

If the math doesn’t scare you, history should. Let’s look at the most recent poster child for the $2 trillion IPO mirage: Saudi Aramco.

When Aramco began its roadshow, the Crown Prince explicitly anchored the target valuation at $2 trillion. But when the physical reality of the business collided with that financial fantasy, the valuation was quietly slashed, and they IPO’d at a fraction of that target.

Why? Because maintaining a $2 trillion illusion requires extreme, sometimes absurd measures.

Take the geological reality of Aramco’s crown jewel, the Ghawar oil field. To keep production numbers looking pristine for the IPO, they had to pump massive amounts of seawater into the aging reservoir to maintain pressure. In doing so, they risked “killing the goose that lays the golden egg,” degrading the long-term viability of the field just to ensure short-term output metrics justified the valuation.

Then came the ultimate stress test. In 2019, Houthi forces from Yemen launched drone strikes that severely damaged the Abqaiq processing facility, knocking out millions of barrels of daily output. Suddenly, Aramco’s core narrative as an unshakeable, reliable global supplier was shattered right before the public listing.

How did they prop up the image? They scrambled to buy oil from Iraq to make up the shortfall and prove to the market that the supply chain was intact. But here is the punchline that Wall Street conveniently glossed over: Iraq, facing its own production and sanction constraints, secretly bought that exact oil from Iran to fulfill the Saudi contract.

Think about that supply chain loop: Saudi Arabia buying from Iraq to look strong, while Iraq buys from sanctioned Iran to fulfill the Saudi order.

Imagine the absolute stunts management will execute to try to prop up a valuation when the operational reality doesn’t match the financial engineering. When you price a company at $2 trillion, you back management into a corner. If Starlink subscriber growth slows, or if Starship faces insurmountable regulatory or technical walls, what financial or operational “stunts” will be pulled to keep the stock price anchored? Will we see aggressive accounting maneuvers, desperate lobbying for inflated government contracts, or strategic illusions to maintain the facade of invincibility?

The “1 Percent” Illusion

This brings us back to the Facebook analogy. When a founder or early insider sells a tiny fraction of their holdings (say, 1%) at a stratospheric price, it creates a “phantom valuation.” It is a marketing tactic designed to anchor public perception.

If I sell you 1% of my house for $20 million, does that mean my house is suddenly worth $2 billion? No. It means you overpaid for a highly illiquid, non-controlling stake, and the implied valuation is detached from the asset’s income-generating reality.

At $2 trillion, SpaceX’s valuation is pricing in perfection. It assumes no regulatory hurdles, no catastrophic launch failures, no disruptive competitors, and infinite capital efficiency. As value investors, we know that “perfection” is not a margin of safety. It is a recipe for disappointment.

The Bottom Line

Price is what you pay; value is what you get.

If SpaceX prices its IPO anywhere near the $2 trillion mark, the math simply does not support an attractive, timely ROI. The denominator is too large. Even with hyper-growth, the time required to generate a compelling return stretches into a decade or more, with significant downside risk if growth merely “normalizes.” And as Aramco proved, when a mega-cap is trapped by an inflated valuation, the operational stunts required to maintain the illusion are as risky as they are absurd.

True value investors do not chase headlines. We wait for the price to come to us. Until SpaceX’s valuation reflects a reasonable multiple of its actual, sustainable free cash flow—with a built-in margin of safety for the inherent risks of the aerospace industry—I will be sitting this IPO out. Let the momentum chasers have the 1 percent illusion. I’ll wait for the intrinsic value.

To achieve the rumored $2 trillion valuation, SpaceX is floating a microscopic fraction of the company. According to recent S-1 disclosures and market reports, SpaceX plans to offer only about 3.3% of its total equity to the public 5.

Here is the breakdown of the numbers behind the IPO structure:

- The Float: The company is floating roughly 3% to 4% of its equity, which analysts have noted makes it the thinnest large-cap float in modern histor.

- The Capital Raise: SpaceX is looking to raise a massive $50 billion to $75 billion war chest to fund its Starship scale-up and expansion.

- The Share Price: At the targeted IPO price of $135 per share, the offering consists of roughly 555.6 million newly minted shares.

- Retail Access: In a highly unusual move, SpaceX is making as much as 30% of these offered shares available directly to retail investors, whereas most IPOs only allocate 5% to 10% of the offering to the public. Additionally, 5% of the IPO shares are being reserved specifically for employees, friends, and family.

The “1 Percent” Illusion in Practice

This structure perfectly illustrates the exact “Facebook valuation” strategy mentioned in the article. By selling just ~3.3% of the company, Elon Musk and the early insiders are able to establish a $2 trillion price tag for the entire business, while retaining roughly 96.7% of the equity in private hands.

This allows the company to extract a record-breaking $50 billion to $75 billion in fresh capital with minimal dilution to the founders. However, it also means the public is buying into an extremely illiquid, tightly controlled asset. The “phantom valuation” of $2 trillion applies to the whole company on paper, but the public only gets to trade the 3.3% sliver, leaving the vast majority of the financial risk and illiquidity locked behind closed doors.

For a value investor, this confirms the ultimate trap: you are paying a massive, hyper-growth premium for a tiny slice of a company whose intrinsic cash flows must now support a $2 trillion anchor, all while the founders maintain absolute control and the public bears the brunt of the market’s volatility.

The Bottom Line

Khawar Nehal is a value investor, technology strategist, and the founder of the Project Equity Method™ (PEM), a framework for outcome-based value sharing in project-driven businesses. He specializes in global business strategy, technology infrastructure, and market valuations, and serves as CTO for multiple international tech ventures.

Contact: khawar@atrc.net.pk

📬 Stay Updated:

If you found this analysis valuable, reply to this email or forward it to a colleague. To ensure you receive my future white papers, market analyses, and technology strategy updates directly to your inbox, please subscribe with the link below.

Disclaimer:

This article is for informational, educational, and commentary purposes only and does not constitute financial, investment, legal, or trading advice. The author is not a registered financial advisor. All investments carry risk, including the loss of principal. The financial figures, IPO terms (including float percentages, share prices, and capital raise targets), and operational details regarding SpaceX and Saudi Aramco mentioned in this article are based on recent private disclosures, S-1 filings, market reports, and historical events, which are subject to change and may not reflect final audited public data. Forward-looking statements and ROI projections are hypothetical scenarios used for analytical purposes and are not guarantees of future performance. Readers should conduct their own due diligence and consult with a licensed financial professional before making any investment decisions.

We strive for the highest level of accuracy in our research and publications. If you find any error to be fixed as a reader, please send updates directly to khawar@atrc.net.pk so they can be promptly reviewed and corrected in future editions.

Update : 13 June 2026 after IPO

- Price-to-Earnings (P/E) Ratio: N/A (Negative due to net losses).

- Price-to-Sales (P/S) Ratio: ~91.5× – 94×.

- Price-to-Book (P/B) Ratio: ~22.6×.

- Profit Margin: ~ -25% to -45% (Net).

- Total Debt to Equity: ~73.6%

![]()